Mortgages are typically repaid over a fixed period of time, usually ranging from 15 to 30 years. Owning a home is a dream for many people, but the high cost can make it seem out of reach. That’s where a mortgage comes in.

By borrowing money from a lender, you can buy a home and pay it off over time. This allows you to spread the cost of the home over several years, making it more affordable. However, it’s important to understand the terms of the mortgage, such as the interest rate and repayment schedule, to ensure you can comfortably manage the monthly payments. In this blog post, we will explore the different types of mortgages, how they work, and provide some tips for finding the right one for you.

Credit: reverse.org

Understanding the anatomy of a mortgage is crucial when it comes to purchasing a home. A mortgage is a loan that is secured by real estate. It allows you to buy a home without having to pay the entire purchase price upfront. Instead, you make monthly payments to the lender over a set period of time, typically 15 or 30 years. In this blog post, we’ll break down the key components of a mortgage and discuss interest rate nuances that you should be aware of There are several key components that make up a mortgage, including:

- Principal: This is the amount of money you borrow from the lender to purchase your home.

- Interest: This is the cost of borrowing money from the lender. It is calculated as a percentage of the principal and is paid back over the life of the loan.

- Term: This is the length of time that you have to pay back the loan. Most mortgages have a term of 15 or 30 years.

- Down Payment: This is the amount of money that you pay upfront when purchasing your home. It is typically a percentage of the purchase price.

The interest rate that you receive on your mortgage can have a significant impact on your monthly payments and the total amount that you pay back over the life of the loan. Here are a few interest rate nuances that you should be aware of:

| Fixed-Rate Mortgage | Adjustable-Rate Mortgage |

|---|---|

| A fixed-rate mortgage has an interest rate that remains the same for the entire life of the loan. | An adjustable-rate mortgage has an interest rate that can change over time based on market conditions. |

| Fixed-rate mortgages are typically more stable and predictable, making them a good choice for those who plan to stay in their homes for a long time. | Adjustable-rate mortgages can be riskier, but they may be a good choice for those who plan to sell or refinance their homes in the near future. |

It’s important to understand the nuances of interest rates when choosing a mortgage. By doing so, you can make an informed decision that best fits your financial situation and long-term goals.

When it comes to getting a mortgage, there are various types to choose from. Understanding the differences between these options can help you make an informed decision that suits your financial needs. Let’s take a closer look at the different types of mortgages available. A fixed-rate mortgage offers a set interest rate for the entire term of the loan, providing stability and predictability in monthly payments. On the other hand, an adjustable-rate mortgage (ARM) usually starts with a lower initial interest rate that may fluctuate over time based on market conditions. Government-Backed vs. Conventional Loans Government-backed loans, such as those offered by the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA), are insured by the government, making them more accessible to borrowers with lower credit scores or limited down payments. In contrast, conventional loans are not insured or guaranteed by the government and typically require higher credit scores and larger down payments.

When it comes to applying for a mortgage, proper preparation is key. Taking the time to gather all the necessary documents and ensure your credit score is in good shape will greatly increase your chances of approval. In this article, we will discuss two important aspects of preparing for a mortgage application: the impact of your credit score and the financial documentation checklist. Your credit score plays a crucial role in determining whether you will be approved for a mortgage and the interest rate you will receive. Lenders use your credit score to assess your creditworthiness and determine the level of risk involved in lending to you. A higher credit score indicates a lower risk and can result in better loan terms. To maintain a good credit score, it is important to make payments on time, keep credit card balances low, and avoid opening too many new accounts. It is also essential to review your credit report regularly for any errors or discrepancies that could negatively impact your score. When applying for a mortgage, you will need to provide various financial documents to verify your income, assets, and liabilities. Having these documents ready ahead of time can streamline the application process and help you avoid delays. Here is a checklist of the essential financial documents you will typically need:

| Document | Explanation |

|---|---|

| Proof of Income | Recent pay stubs, W-2 forms, or tax returns |

| Bank Statements | Statements from your checking, savings, and investment accounts |

| Proof of Assets | Documentation for any other assets, such as real estate or vehicles |

| Employment Verification | Confirmation of your current employment status and income |

| Debt Information | Details of your outstanding debts, including credit cards, loans, and mortgages |

By gathering these documents in advance, you can be well-prepared for the mortgage application process and provide the necessary information to lenders in a timely manner.

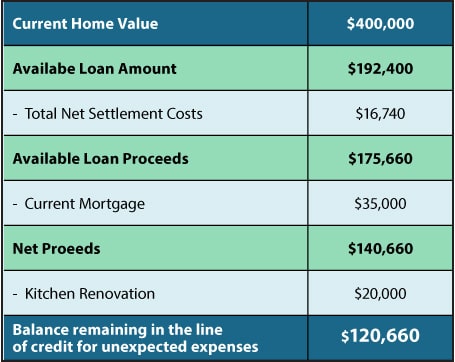

Calculate what you can afford for a mortgage with this example. Start by determining your monthly income and expenses to gauge what monthly mortgage payment you can comfortably handle. Then, use an online mortgage calculator to estimate the potential costs.

Calculating What You Can Afford: When it comes to applying for a mortgage, one of the most important factors to consider is how much you can afford to borrow. Calculating what you can afford involves assessing your income, expenses, and down payment options. In this section, we will discuss the income to debt ratios and down payment considerations that will help you determine how much you can afford to borrow. Income to Debt Ratios: Lenders use income to debt ratios to determine how much you can afford to borrow. This ratio compares your monthly debt payments to your monthly income. The two ratios that lenders use are the front-end ratio and the back-end ratio. By considering these factors, you can determine how much you can afford to borrow and make an informed decision about your mortgage options.

Smart Borrowing Tips

When considering a mortgage, it’s essential to be a savvy borrower. Here are some smart tips to help you navigate the process effectively.

Shopping For The Best Rates

Compare rates from different lenders to get the best deal.

Understanding Loan Estimates

Review loan estimates carefully to grasp all associated costs.

Strategies For Paying Off Your Mortgage Sooner

When it comes to homeownership, one of the top financial goals for many individuals is to pay off their mortgage as quickly as possible. By implementing effective strategies, you can work towards becoming mortgage-free sooner than expected. Let’s explore some key strategies for paying off your mortgage sooner.

Extra Payments

One effective strategy for paying off your mortgage sooner is by making extra payments. By increasing your monthly payment amount or making additional payments towards your principal balance, you can significantly reduce the overall interest paid and shorten the life of your loan.

Refinancing Options

Considering refinancing options can be another valuable strategy for paying off your mortgage sooner. Refinancing to a shorter loan term or a lower interest rate can help you save on interest costs and accelerate the payoff timeline.

Mortgage Pitfalls To Avoid

Mortgages can be complex, and it’s crucial to navigate the process carefully to avoid common pitfalls. Being aware of Common Borrower Mistakes and Predatory Lending Practices can help you make informed decisions when securing a mortgage.

Common Borrower Mistakes

- Overspending on a property beyond financial means.

- Not shopping around for the best mortgage rates.

- Ignoring additional fees and closing costs.

Predatory Lending Practices

- Excessive fees and high-interest rates.

- Unnecessary insurance or add-on products.

- Unfair terms and conditions that benefit the lender.

Credit: www.researchgate.net

Navigating Mortgage Challenges

When faced with mortgage challenges, it’s essential to understand the available options for navigating through difficulties.

Handling Financial Hardship

If financial hardship arises, communicate with the lender promptly to explore solutions.

Loan Modification And Assistance Programs

Seek assistance through loan modification programs or financial support initiatives.

Investing In Real Estate Through Mortgages

Investing in Real Estate through Mortgages can be a lucrative opportunity.

Leveraging Property Investments

Leverage property investments by utilizing mortgage financing options.

Rental Income And Mortgage Payments

Generate rental income to cover mortgage payments and build equity.

Future Trends In Mortgage Lending

The mortgage industry is rapidly evolving, with several key trends shaping the future of mortgage lending. From advancements in technology to changing regulations and their impact on borrowers, staying informed about these developments is crucial for anyone looking to navigate the world of mortgages successfully.

Technology In Mortgage Processing

Advancements in technology are streamlining the mortgage application process, making it faster and more efficient.

Changing Regulations And Borrower Impact

Regulations governing mortgage lending are constantly evolving, impacting both lenders and borrowers. Understanding these changes is essential for borrowers to navigate the lending landscape successfully.

Credit: www.consumerfinance.gov

Frequently Asked Questions

What Is An Example Of A First Mortgage?

A common example of a first mortgage is when a homebuyer borrows money from a bank to purchase a house.

What Is A Mortgage Easy Way To Explain?

A mortgage is a loan used to purchase a home or property. The borrower agrees to pay back the loan plus interest over a set period of time. The property is used as collateral, which means the lender can seize it if the borrower fails to repay the loan.

Is A Mortgage An Example Of Credit?

Yes, a mortgage is an example of credit. It allows individuals to borrow money to purchase a property and repay it over time. A mortgage is a form of loan secured by the property itself.

How Does Mortgages Work?

Mortgages work by borrowing money to buy a home, which is paid back over time with interest. You make monthly payments, and the lender holds the property as security until the loan is fully repaid. If you miss payments, the lender can take possession of the property.

Conclusion

Understanding the concept of a mortgage is crucial when considering homeownership. By grasping the key components such as interest rates, loan terms, and down payments, individuals can make informed decisions that align with their financial goals. Remember to carefully evaluate your options, seek professional advice if needed, and choose a mortgage that suits your unique circumstances.

With this knowledge, you can navigate the mortgage process confidently and embark on the path to owning your dream home.